In this article, we look into another question our Strata Managers are asked on a regular basis – ‘What does our Strata Insurance cover?’

It is a legal requirement under the Strata Act in NSW that all Owners Corporations of a Strata Scheme insure the building and keep the building insured under a contract of insurance against fire, lightning, explosion and any other occurrence specified in the policy. Such insurance also covers the common property, which in many instances would include items such as gardens, driveway, carparks and pools.

What is covered by building insurance?

The definition of ‘building’ for the purposes of a strata scheme is the structure shown on the Strata Plan. The insurance also extends to those items outlined as requiring coverage under the Strata Schemes Management Act 2015.

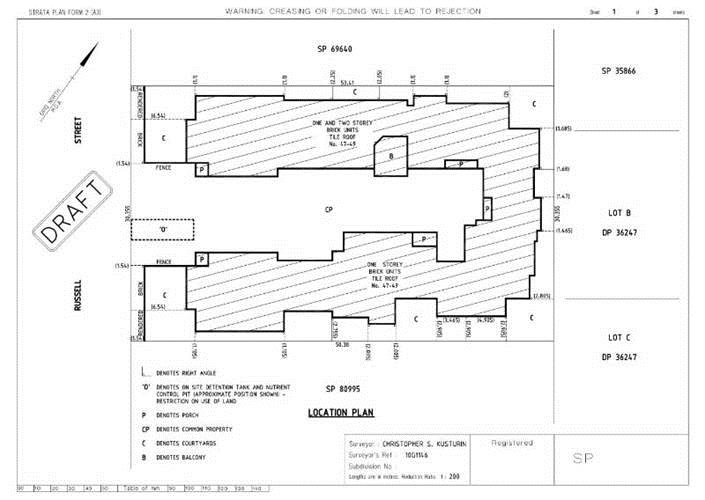

Below is an example of a Strata Plan:

Those items shown in a thick black line are considered common property (structure) and are covered as part of the ‘Building Sum Insured’, including the roof and its roof cavity. Items labelled ‘CP’ (Common Property) would also be covered under the building insurance.

As Strata Managers the most common claims relating to common property include:

- Storm damage, in particular hail damage to tile and colourbond roofs.

- Damage caused by leaking or burst pipes within common walls – infrastructure such as wiring and service pipes found in common area spaces are typically considered common property.

- Accidental impact damage to glass – rocks flicked up, wind slamming doors etc.

- Malicious damage to common property – graffiti and theft unfortunately frequently affect common property.

- Although not as common as other causes, fire has the potential to cause substantial damage to common property.

- Given the variety of potential claims, it is imperative that adequate cover is in place for your Strata Scheme. You may have noticed on your AGM agenda that Strata North recommend the Owners Corporation obtains a valuation at least every 3 years – this is the best way to ensure the Owners Corporation is adequately covered.

Other inclusions regularly found within a Strata Insurance Policy

Lot Owners Fixtures and Additions

As a strata owner it is important to know that insurance companies who provide strata insurance may extend coverage to include “Lot Owners Fixtures and Additions.” This means those permanent fixtures within a Lot would be covered in the event they are damaged by an insurable event.

These items would generally be excluded from coverage in your contents/landlords insurance if already covered under the Owners Corporation’s insurance policy but it is recommended that owners check this with their contents insurer.

CHU Insurance (2019) in their Contents Fact Sheet included the below diagram explaining what items are covered by their strata insurance policy and what is not covered:

Accordingly, you should check that the policy held by your Owners Corporation includes Lot Owners Fixtures and Additions.

Although an item would normally be covered by the Owners Corporation’s insurance policy, owners may need to consider the following:-

- A by-law does not exist at the complex conferring responsibility for the item to the unit owner.

- The installation has the appropriate approvals e.g. Council and/or Owners Corporation.

- Damage is caused by an insurable event and is accidental in nature.

Public Liability Insurance

The Strata Schemes Management Regulation 2016 requires an Owners Corporation to have Public Liability Coverage in place for a minimum $20 million.

This will protect the Owners Corporation if an incident were to take place on common property causing harm to person or property.

Loss of Rent

This protects the financial interest of both:

- Owner Investors – those owners who rent out their lot will be provided coverage for any lost rent (up to the policy limit) should their Lot be damaged by an insurable event and deemed uninhabitable by the insurer. The insurer pays the owner the amount of rent that the tenant would normally pay, and the tenant, instead of paying the owner, will use that money to fund alternate accommodation.

- Owner-occupiers – should a Lot be deemed uninhabitable by an insurable event the owner-occupier will be paid market rent to Let their property and use that revenue to pay for alternate accommodation whilst the property is being repaired.

The amount of lost rent will be paid to the owner until the lot is no longer uninhabitable in accordance with the amount referred to in the policy. Commonly, the level of cover is 15% of the building sum insured. For example, should the building be insured at $3,000,000 there would be loss of rent coverage of $450,000 per claim.

It is important to note that the tenant’s costs or losses which they may suffer as a result of having to move out of the lot are not normally covered.

Voluntary Workers Compensation

This provides protection to any person who works voluntarily on behalf of the Owners Corporation and becomes injured in the process of undertaking this work. Owners should notify the strata manager if they intend to undertake unpaid work so we can make a note on the policy with the insurer.

Office Bearers Liability Insurance

This type of insurance protects the Owners Corporation against any loss suffered as a result of a wrongful act committed by a Strata Committee member in the course of undertaking their duties.

Hopefully this article has helped to clear up some of your questions around Strata Insurance.

Regards,

Strata North

Note: this is informal advice and if you have any specific queries, we are happy to seek clarification from your strata building insurer.